The Impact of Donald Trump’s Election Promises on Global Oil & Geopolitics?

Among notable promises made by US President-elect Donald Trump during his presidential elections were four particular ones that attracted the attention of the world because of their geopolitical implications and their impact on the price of oil. These were the dismantling of the nuclear deal with Iran, lifting the sanctions on Russia, enhancing US oil production and a strong dollar.

Whilst most declarations made by US presidential candidates during their election campaigning would be quickly forgotten once they are installed inside the White House, it might be wise to analyse these promises in case Mr Trump stuns the world by fulfilling some or all of them.

Will Donald Trump Dismantle the Iran Nuclear Deal?

U.S. President-elect Donald Trump has vowed to rip up the Iranian nuclear agreement on Day 1 and re-install sanctions on Iran.1The move could potentially have far-reaching geopolitical consequences for the United States, the Arab Gulf region and the global oil markets.

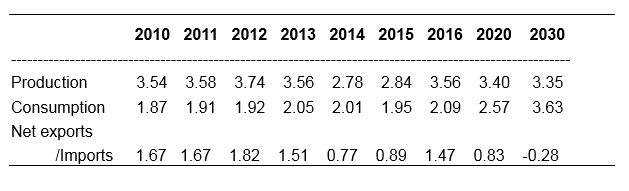

The 2015 deal between the P5+1 nations (US, France, the UK, Russia, China and Germany) and Iran was one of the signature achievements of the Obama administration, one that produced multiple benefits. First, it significantly reduced tension between Iran and the US, a relationship that had become so hostile in the preceding years that the drumbeats of war could be heard in Washington. Second, the agreement put restraints on Iran’s nuclear program. For Iran, the deal also paved the way for a return to international markets and allowed it to ramp up oil production and exports. All told, Iranian oil exports had dropped from 1.67 million barrels a day (mbd) in 2011 to just 0.89 mbd by 2015. Iran has since restored much of that lost output (see Table 1).

Table 1

Iran’s Current & Projected Crude Oil Production,

Consumption, Exports & Sustainable Capacity, (2010-2030)

(mbd)

Sources: IEA’s World Energy Outlook 2015 / BP Statistical Review of World Energy, June, 2016/ OPEC Annual Statistical Bulletin 2016 / Author’s Estimates.

There are not many issues on which Europe, Russia and China all agree, but there is one: ensuring that President Trump does not undermine the Iran nuclear deal.

There are legitimate grounds for concern that Donald Trump’s administration or Congress could sabotage the deal to which Mr Trump has referred as a “disaster” and vowed to dismantle. The president-elect has also surrounded himself with people like Rudolph Giuliani and John Bolton, who have said they want an immediate end of the deal. Mr Trump’s pick to lead the CIA, Mike Pompeo, recently said he looks to rolling back this disastrous deal with the world’s largest state sponsor of terrorism.2

As Mr Trump decides in what direction he will take his Iran policy, countries that have partnered with the United States on Iran must draw a line. They should firmly tell the president-elect that as long as Iran continues to meet its obligations under the deal, they will do so as well. They should also make clear that if either Congress or the American president unravels the deal, other world powers will go their way with Iran.

There is a good chance that after intelligence briefings show Mr Trump how United States’ security interests have benefited from the deal, he will come to realize the importance of keeping it intact.

But Mr Trump may also be persuaded by the hawks with whom he has surrounded himself to swiftly deliver a death blow to the deal by seeking to renegotiate American commitments on easing sanctions. This could result in the re-introduction of secondary US sanctions against international companies doing business with Iran.

However, some countries, including American allies in Europe and Asia could reject the Trump administration’s demands. As such, oil flows would be re-routed from countries that comply with Washington’s demands to those that refuse to comply. If a major oil importer like China decides not to cooperate with President Trump, the US effort to contain Iran will likely fail.

It will be Mr Trump, as president, who will have to deal with these repercussions. Because the international coalition that previously supported sanctions on Iran will not be put back together, America’s economic leverage on Iran will be much weaker, increasing the likelihood that Iran will ramp up its nuclear programme and, in turn, increasing the risk of American military action.

On November 14, 2016, 28 European leaders unanimously reiterated their “resolute commitment” to the deal regardless of the outcome of the American elections. Heads of state from the five countries that negotiated the deal with Iran would undoubtedly feel personally betrayed by the American president’s withdrawal. This is likely to put the United States in a confrontation with Russia, China and Europe not just on Iran but on other issues such as the Islamic state, the war in Syria and North Korea, where Mr Trump needs their cooperation.

Walking away also would leave the U.S. with few options outside a military strike to curtail Iran’s nuclear ambitions because European powers probably wouldn’t agree to return to the crippling sanctions regime that Tehran previously faced.

Central Intelligence Agency Director John Brennan told BBC last month that it would be “the height of folly if the next administration were to tear up that agreement.”

So, it seems likely that the deal will remain in place. The alternative is a war with Iran prompted by Israel, which the United States neither can afford nor can win without using tactical nuclear weapons.

For the global oil market, dismantling Iran nuclear deal will hamper Iran’s efforts to rebuild its ailing oil industry. Even without sanctions, it will take Iran more than 3-5 years and $200 bn of investments to repair the damage in its reservoirs, according to the International Energy Agency (IEA).3

For oil prices, a reduction in Iran’s oil exports resulting from a possible re-introduction of American sanctions, could lead to a tighter global oil market and push oil prices steeply upward. However, the geopolitical risk would arguably be more important. It could heighten tensions between Saudi Arabia and Iran, which could escalate to war that would engulf the whole region.

Iran’s Defence Minister Hossein Dehgan was quoted by Reuters News Agency saying that “enemies may want to impose a war on Iran but if such a war were to occur it will mean the destruction of Israel and will engulf the whole Gulf region”.4

Saudi Arabia and other Gulf Cooperation Council (GCC) Countries view Iran’s nuclear programme as a smokescreen for developing nuclear weapons. This, they believe, poses the greatest challenge to their oil wealth and strategic security.5

In balancing Iran’s power it is tempting for Saudi Arabia to turn to nuclear weapons as part of a larger strategy to counter Iranian influence. Saudi leaders are on record suggesting that the Kingdom would counter nuclear Iran by acquiring nuclear weapons too.6

Lifting the Sanctions on Russia

President Obama established the current Ukraine-related sanctions on Russia in 2014 through executive orders that Mr Trump could undo with the stroke of a pen.

Senate democrats are powerless to stop Donald Trump from easing or lifting Ukraine-related sanctions against Russia after he takes office. Their outcry on sanctions could become a shriek this year as confirmation hearings begin for Exxon Mobil CEO, Rex Tillerson, whom Mr Trump picked for secretary of state. Mr Tillerson would bring close ties to Russian president Putin and an open scepticism of sanctions as a policy tool to a Trump administration that wants to collaborate with Russia on fighting the Islamic State.

Democrats are worried that if the Trump administration weakens sanctions against Russia, the European Union could move to follow suit, imperilling the entire effort. And whilst the United States and Russia are not large trade partners, the European Union does an enormous amount of trade with Russia. More than 50% of Russian exports of goods went to EU countries in 2014, according to the Congressional Research Service.

Putin is not interested in a reset with the Trump administration that doesn’t involve the lifting of sanctions. Putin hopes that he and Donald Trump can work together to end the crisis in Russian-American relations as well as address the pressing issues of the international agenda and the search for effective responses to global security challenges.

Russia has more than $8 trillion worth of untapped oil and gas, but it needs sophisticated Western technology and services to actually extract it. In the run-up to 2014 sanctions, Exxon Mobil, led by Mr Tillerson, and Russia’s oil giant Rosneft invested $3.2 billion in a project for drilling for oil in the Kara Sea in the Arctic — a region that Rosneft estimated it could have more oil than the entire Gulf of Mexico. But the sanctions forced Exxon Mobil to halt drilling.7Moreover, Russia estimated that Western sanctions cost its economy in 2015 more than $100 bn – by now, it is likely to have cost many billions more.8

Exxon Mobil’s involvement in the Russian Arctic could have a very significant impact on the global oil market and prices in that it could, in a few years, add more than 1.5 mbd to Russia’s current oil production of 11.2 mbd thus consolidating Russia’s position as the top oil producer in the world.9

And while nobody can predict which direction Trump’s policy vis-à-vis Russia will take, his nomination of Mr Tillerson for the post of US Foreign Secretary could be a clear sign of intent that Mr Trump may be considering easing if not lifting sanctions on Russia.

Enhancing US Oil Production: Donald Trump’s Vision

Donald Trump aims to increase US oil production and make the United States a powerful voice in the global oil Market along Saudi Arabia and Russia. This objective would certainly be made easier with the projected rise in oil prices as a result of the OPEC and non-OPEC oil producers’ agreement to cut production by almost 1.8 mbd. Rising oil prices will enhance US shale oil production.

Donald Trump believes that shale oil production could make the United States self-sufficient in oil and could also add 2 million new jobs in 7 years. He considers America’s energy dominance a strategic economic and foreign policy goal. Mr Trump also wants to unleash America’s estimated $50 trillion in untapped shale oil and natural gas reserves.10To achieve this objective Mr Trump plans to ease the process for leasing federal lands. Overall, the impact of Trump’s oil policies is likely to be small. Most shale oil production relies on private lands (or public leases), and the regulatory apparatus for oil and gas won’t change much. In 2014, only 21% of US oil production and 14% of gas came from federal lands, according to the most recent data from the Energy Information Administration.

On balance, US oil production will not increase much above the current 8.77 mbd. A recent Columbia University report estimates that US shale would see an increase in output of 300,000 to 900,000 barrels a day (b/d) in the next few years taking total production to 9-10 mbd if oil prices rise above $60 per barrel.11Moreover, any increase in US shale oil production of such magnitude will have little impact on the oil price in view of the recent production cuts by OPEC and non-OPEC producers.

The United States will never achieve oil self-sufficiency and will remain a major oil importer for the foreseeable future to the tune of 7-8 mbd.

Enhancing the Value of the US Dollar

Following the election of Donald Trump, the dollar surged 2% in value against the Chinese Yuan and a 3.1% against a basket of 10 leading global currencies.12

The dollar’s strength has been especially dramatic against the Chinese Yuan, which Trump repeatedly targeted in his campaign, accusing the Chinese government of currency manipulation to benefit its economy.

The weaker Yuan and stronger dollar could be a gain for US consumers and businesses buying goods made in China. On the flip side, when the dollar is strong, US exports become less competitive and more expensive for the Chinese to buy. This divergence could lead to calls to impose tariffs and also set the stage for the return of protectionist rhetoric.

Investors expect Mr Trump’s proposals to boost fiscal spending, cut taxes and loosen regulation will bolster economic growth and ultimately prompt the Federal Reserve to step up the pace of short-term interest-rate hikes. Investors say the biggest boon for the dollar could be higher US interest rates. Mr Trump’s plans for big fiscal spending are expected to boost inflation and bolster the case for lifting US rates.13

During the presidential campaign, Mr Trump threatened to slap tariffs on countries like China, which he claims are gaining an unfair trading edge due to poor trade deals or purposely depressing their currencies. But tariffs could cause problems as consumers lose the benefit of lower prices while the US might not gain much. In retaliation, China could liquidate its holdings of US Treasury bills estimated at $1.2 trillion pushing US interest rates higher, tilting both countries into recession and possibly engaging in a trade war. Meanwhile, the possibility of a Chinese/US military confrontation in the South China Sea grows.

Trump’s vow to borrow and spend on domestic projects has helped push interest rates to their highest levels of the year as investors expect the Trump administration to sell Treasury bills to finance its domestic spending. China and Japan are major buyers of US debt and they will be needed to finance US planned domestic spending. However, the US economy is already facing a high level of indebtedness estimated currently at almost $20 trillion (107% of GDP).14This suggests that any change in monetary policy would have to be carried out in a gradual manner and that any corresponding strengthening would be gradual.

What is, however, certain is that a strengthening of the US dollar will also equally strengthen the petrodollar by which oil is priced and sold worldwide.

Raising the value of the dollar exerts a downward pressure on oil prices. On the other hand, by devaluing the petrodollar at any point in time, the actual purchasing power of the oil revenues of OPEC and non-OPEC oil producers, declines against other world currencies. This would cause inflation because the value of the petrodollar vis-à-vis other world currencies will also decline. In other words, the trade balances of the oil-producing countries with the rest of the world deteriorate causing them to spend more of their revenues on imports and this pushes inflation up. 15

Conclusions

Even if Donald Trump’s electioneering promises were to be fulfilled, their impact on the global oil market and the price of oil would be limited if not insignificant. However, the geopolitical impact would reverberate throughout the globe with rising tension between China and the United States and also between Iran and the GCC countries that has the potential to escalate to war.

As for global oil, any upward pressure on oil prices and a tightening of the global oil market resulting from the dismantling of the Iran nuclear deal would be offset by the extra oil production coming from Russia’s arctic region.

Equally, any increase in US shale oil production would be undermined by a decline in global oil demand resulting from the rising value of the dollar against other currencies. This will exert a downward pressure on the oil price thus leading to a reduction in shale oil production and rising production costs.

*Dr Mamdouh G. Salameh is an international oil economist. He is one of the world’s leading experts on oil. He is also a visiting professor of energy economics at the ESCP Business School in London.

The views and opinions expressed in this article are those of the author and do not necessarily reflect the position of ESCP Business School.

Useful links:

ESCP Business School

Executive Master in Energy Management

MSc in Energy Management

Footnotes

1- Nick Cunningham,“What Happens to Oil if Trump Tears Up Iran NuclearDeal?”Oilprice.com,23 November, 2016, accessed on 6 January 2017.

2- Ellie Ceranmayeh, “Will Donald Trump Destroy the Iran Deal”, published by the New York Times on November, 2016.

3- Mamdouh G Salameh, “A Nuclear Iran Poses Real Threat to Oil Resources & Strategic Security of the GCC Countries”(a Paper given at the Arab Centre for Research & Policy Studies’ Gulf Studies Forum, December, 5-7, 2015, Doha, Qatar).

4- Reuters News Agency, 13 December, 2016.

5- Mamdouh G Salameh, “A Nuclear Iran Poses Real Threat to Oil Resources & Strategic Security of the GCC Countries”.

6- A. Alsharif & A. McDowall, “Saudi Prince Turki Urges Nuclear OptionAgaintIran”, Reuters, December 6, 2011.

7- www.vox.com accessed on 3 January 2016

8- Ibid.

9- Estimated on the basis of current US oil production of 8.77 mbd and data from the US Energy Information Administration (EIA) showing that the Gulf of Mexico contributes 17% to total US oil production.

10- An America First Energy Plan: Donald Trump’s Vision, www.donaldjtrump.com/policies/energy, accessed on 7 January 2017.

11-A Report by The Centre on Global Energy Policy, Colombia University, published December 2016.

12-Chelsey Dulaney, “US Dollar Rally Finds New Life under Trump”, Wall Street Journal, 13 November, 2016.

13-Ibid.

14-Data from the Bureau of Economic Analysis (BEA) of the US Department of Commerce.

15-Saudi Arabia’s Oil Strategy & Its Impact on Oil Prices” (A presentation at the

Regional Oil Conference organized by the Arab Administrative Development

Organization (ARADO) of the Arab League, 17-18 May 2016, Cairo, Egypt).

Facebook

Facebook Linkedin

Linkedin Instagram

Instagram Youtube

Youtube EMC Newsletter

EMC Newsletter